- HOME

- Sustainability

- Addressing Climate Change and Nature-related Issues (TCFD, TNFD)

Addressing Climate Change and Nature-related Issues (TCFD, TNFD)

Introduction (our approach to environmental issues including climate change and natural capital)

The SCB has formulated the “Declaration of Shinkin Central Bank Group on SDGs” and, as the central financial institution of all shinkin banks, is working towards the realization of a sustainable society together with shinkin banks across country, focusing on the three important pillars of “community,” “people” and “environment,” in accordance with the mutual aid and non-profit principles of a cooperative organization.

The SCB has formulated the “SCB Group Environmental Policy” to address environmental issues including climate change and natural capital and is actively working to resolve these issues through its operations and other activities.

In addition, the SCB endorsed the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and Task Force on Nature-related Financial Disclosures (TNFD). Information is disclosed in line with TCFD and TNFD recommendations as follows.

Governance

-

Policies regarding sustainability, including climate change and natural capital, are discussed at the Executive Committee and then resolved at the Board of Directors.

The progress of initiatives based on the policies of the Board of Directors is discussed at the Executive Committee and reported to the Board of Directors at least once a year.

We regularly submit climate change risks for discussion at committees such as the Risk Management Committee, a subordinate body of the Executive Committee, and other committees.

In addition, from the standpoint of integrated management as one banking group, we hold the “Group Sustainability Promotion Committee” meetings twice a year, a committee comprised of President and CEO as well as the Director in charge of Sustainability Promotion Division of the SCB and group company presidents to discuss such matters as the SCB Group’s policies and initiatives regarding sustainability.

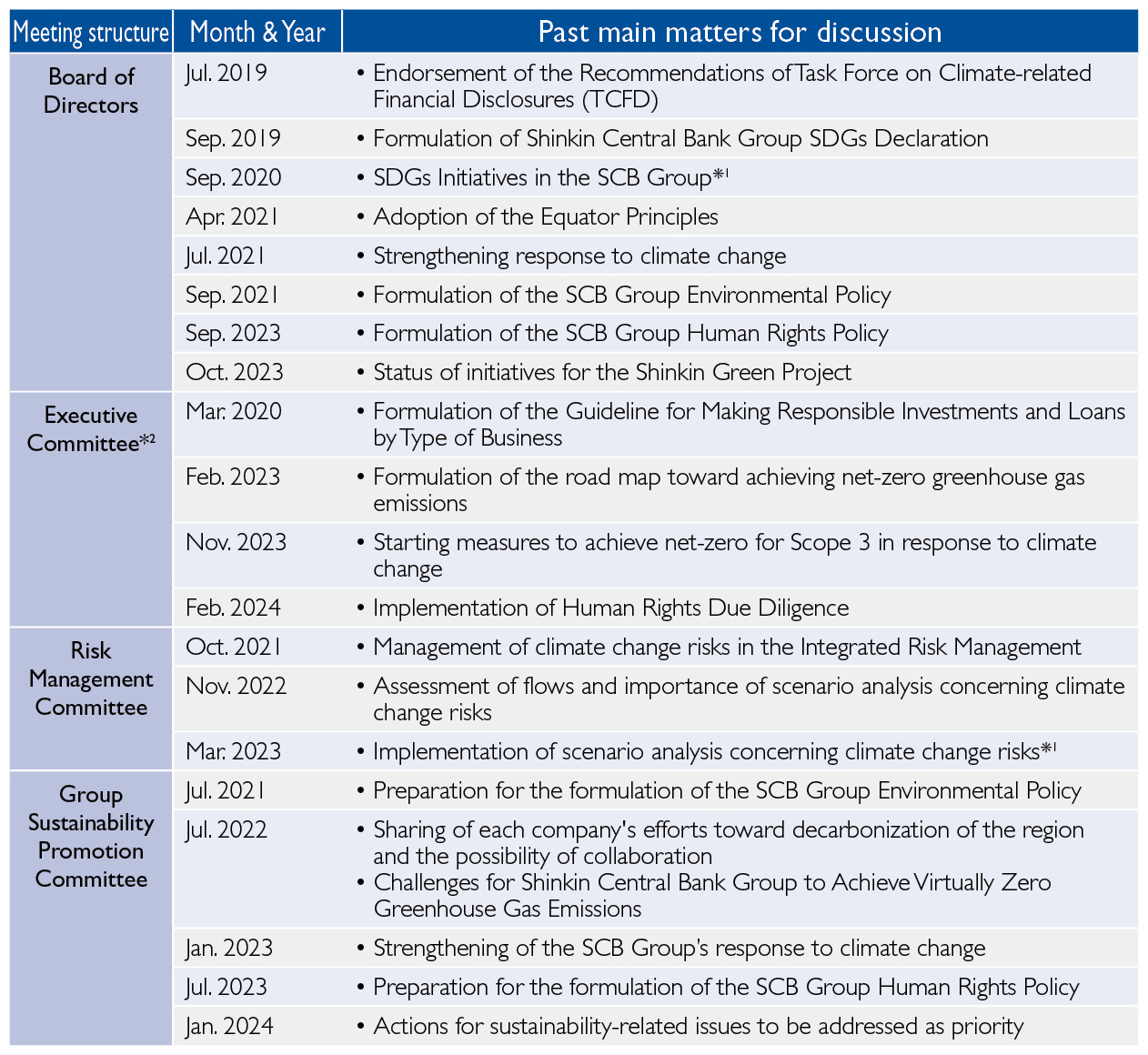

Meeting structure Month & Year Past main contents for discussion Board of Directors Jul. 2019 Endorsement of the Recommendations of Task Force on Climate-related Financial Disclosures (TCFD) Sep. 2019 Formulation of the Declaration of Shinkin Central Bank Group on SDGs Sep. 2020 SDGs initiatives in the SCB Group*1 Apr. 2021 Adoption of the Equator Principles Jul. 2021 Strengthening response to climate change Sep. 2021 Formulation of the SCB Group Environmental Policy Sep. 2023 Formulation of the SCB Group Human Rights Policy Oct. 2023 Status of initiatives for the Shinkin Green Project Sep. 2024 Progress of sustainability initiatives of the SCB Group Jan. 2025 Formulation of Medium-Term Management Plan (including identification of materiality for the SCB Group) Mar. 2025 Endorsement of the Recommendations of Task Force on Nature-related Financial Disclosures (TNFD) Executive Committee*2 Mar. 2020 Formulation of the Guideline for Responsible Investments and Loans by Type of Business Feb. 2023 Formulation of the road map toward achieving net-zero greenhouse gas emissions Nov. 2023 Starting measures to achieve net-zero Scope 3 in response to climate change Feb. 2024 Implementation of Human Rights Due Diligence Sep. 2024 The goals of the Shinkin Green Project set for 2030 Oct. 2024 Initiation of measures in line with the TNFD recommendations Nov. 2024 Progress toward achieving Scope 3 net zero Jan. 2025 Establishment of sustainable finance standards and medium- to long-term target amounts Risk Management Committee Oct. 2021 Management of climate change risks in the Integrated Risk Management Nov. 2022 Assessment of flows and importance of scenario analysis concerning climate change risks Mar. 2023 Implementation of scenario analysis concerning climate change risks*1 Group Sustainability Promotion Committee Jul. 2021 Preparation for the formulation of the SCB Group Environmental Policy Jul. 2022 Sharing of each company’s efforts toward decarbonization of the region and the possibility of collaboration

Challenges for the SCB Group to achieve virtually zero greenhouse gas emissionsJan. 2023 Strengthening the SCB Group’s response to climate change Jul. 2023 Preparation for the formulation of the SCB Group Human Rights Policy Jan. 2024 Actions for sustainability-related issues to be addressed as priority Jul. 2024 Preparation for the identification of materiality for the SCB Group Jan. 2025 Measures to achieve positive impact - *1

- Topics that are regularly submitted for discussion are listed only once when it is submitted for the first time.

- *2

- Topics for the Executive Committee that are submitted to the Board of Directors after deliberation at the Executive Committee are omitted.

- Initiatives for sustainability, including climate change and natural capital,are being taken cross-organizationally, with the Sustainability Promotion Division playing a central role.

- We invited experts in natural capital to lead a study session for directors and other officers on initiatives related to natural capital and biodiversity in local community financing services.

Initiatives for nature-related stakeholders

- We have formulated the “SCB Group Human Rights Policy,” conducted human rights due diligence and identified “impacts on original inhabitants, regional community residents and the environment” as one of the human rights issues.

- Addressing natural capital is an important issue for shinkin banks that are rooted in their communities and grow alongside them. As the central financial institution for shinkin banks, we are working with shinkin banks to solve issues in the regional communities.

Strategy

Opportunities Associated With Climate Change

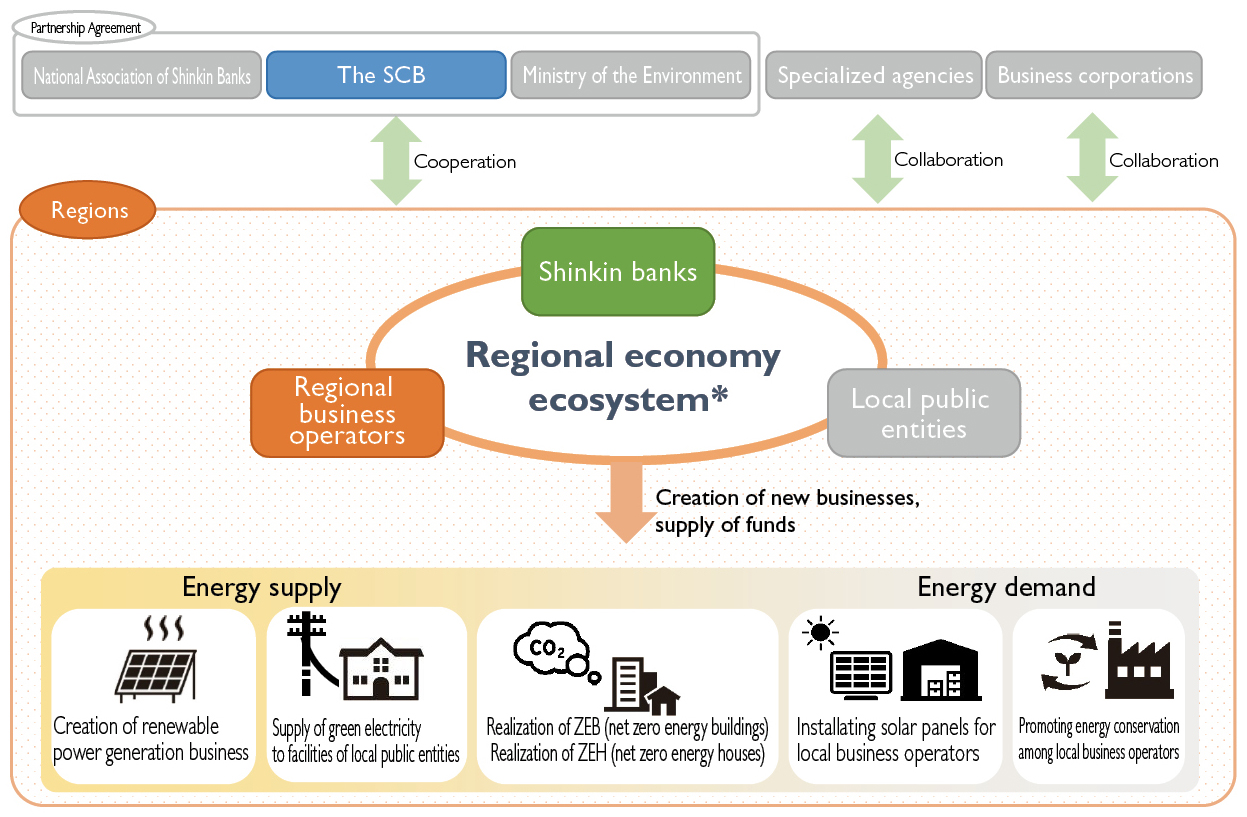

The SCB Group has specified “development of local industries and Japan’s growth” and “collaborating with regional communities on environmental issues” as key social issues (materiality). Through its business activities, the group aims to enhance corporate value while achieving social impact by contributing to a sustainable society through finance and promoting the decarbonization of regional communities and SMEs.

Specifically, these activities include the promotion of sustainable finance and the “Shinkin Green Project.”

- Viewing the expansion of renewable energy and advancements in technology as investment opportunities, we are committed to promoting sustainable finance that contributes to the solution of environmental and social issues, including climate change, with a medium- to long-term goal of a cumulative total of ¥5 trillion by 2030 (covering the period from fiscal 2021 to fiscal 2030).

-

We recognize that encouraging decarbonization initiatives in regions and SMEs will not only lead to new businesses and growth opportunities for SMEs, but is also important from the perspective of revitalizing regional economies.

Together with shinkin banks nationwide, the Green Project Promotion Office in the Sustainability Promotion Division, is taking the lead in promoting initiatives such as regional decarbonization in cooperation with government agencies and external organizations.

Risks Associated With Climate Changes

We recognize that potential climate change risks associated with the transition to a low-carbon society, such as stronger climate-related regulations and technological innovations (transitional risk), and risks associated with physical damage caused by natural disasters and increased abnormal weather due to climate change (physical risk).

As these risks are expected to have a direct impact on our business activities and an indirect impact through the effects on our investment and lending destinations, we are establishing a business continuity system and addressing the impact on the SCB’s finances.

- In providing financial functions required to maintain the economic activities of shinkin banks and other stakeholders, we, as the central bank for shinkin banks, have formulated our business continuity plan (BCP) assuming the risks in which natural disasters would have a material impact on performing our business and put a structure in place that enables us to continue essential businesses when these become apparent.

-

In order to quantitatively evaluate the impact on the SCB’s finances of impact of climate change on investment and lending recipients, we conducted the following scenario analysis.

Scenario Analysis for Climate Change

Based on the “Practical Guide for Scenario Analysis of Climate Change Risks and Opportunities in Accordance with TCFD Recommendations (for the Banking Sector) ver.2.0” released by the Ministry of the Environment, we analyzed two scenarios: “1.5°C” and “4°C.”

Additionally, the exposures covered by the analysis were limited to loans, in line with the TCFD recommendations.

(i) Organization of worldview per scenario

The worldviews of the 1.5°C and 4°C scenarios are as follows. In understanding the risks of each scenario, short-term, medium-term, and long-term timescales are set as the time spans to be addressed.

[Worldview of the 1.5°C scenario]

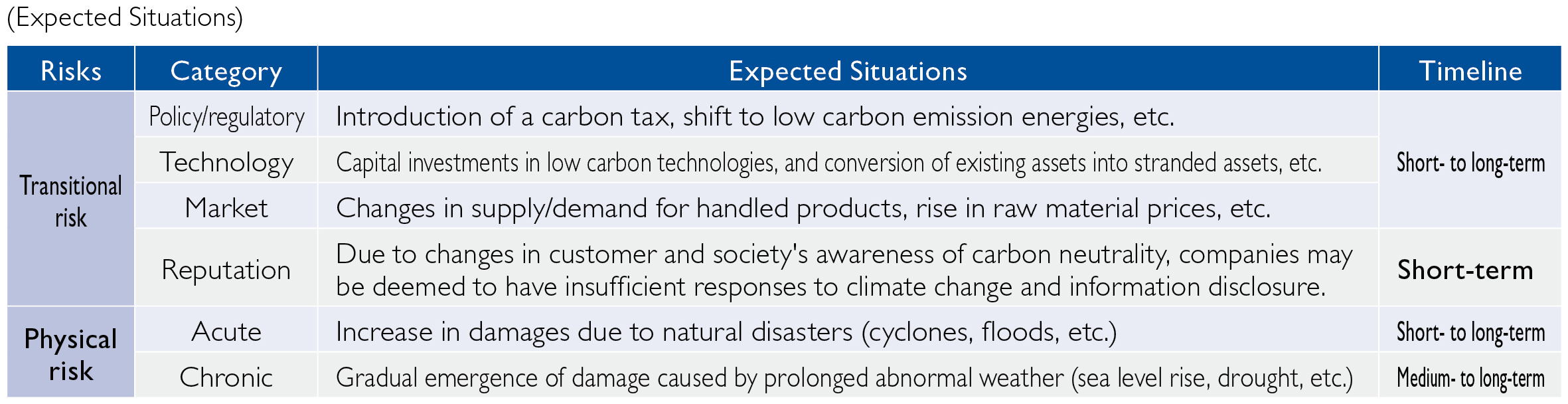

Towards achieving net zero by 2050, strict measures have been taken in “policy-based legal regulations,” and awareness is changing throughout society

(Expected situations) Risks Category Possible Situations Timeline Transitional risk Policy/regulatory Introduction of a carbon tax, shift to low carbon emission energies, etc. Short- to

long-termTechnology Capital investments in low carbon technologies, and conversion of existing assets into stranded assets, etc. Market Changes in supply/demand for handled products, rise in raw material prices, etc. Reputation Due to changes in customer and society’s awareness of carbon neutrality, companies may be deemed to have insufficient responses to climate change and information disclosure. Short-term Physical risk Acute Increase in damages due to natural disasters (cyclones, floods, etc.) Short- to

long-termChronic Gradual emergence of damage caused by prolonged abnormal weather (sea level rise, drought, etc.) Medium- to

long-term- (Expected Impacts)

-

The risks associated with the transition to a low-carbon society (transitional risk), such as tighter climate-related regulations and technological innovation, will increase and affect the businesses and financial conditions of investment and loan customers, which can be expected to affect a portfolio indirectly.

At the same time, physical risks are assumed to be lower than those in the 4°C scenario.

[Worldview of the 4°C scenario]

No major changes in the mindset of the entire society as actions under “laws and regulations based on policy” toward net zero by 2050 are insufficient, and disasters become more severe

(Expected situations) Risks Category Possible Situations Timeline Transitional risk Actions toward net zero in each category and change in mindset are assumed to be insufficient compared to those in the 1.5°C scenario -*1 Physical risk Acute Natural disasters (cyclones, floods, etc.) become more severe and damages increase significantly compared to the 1.5°C scenario Medium- to long-term Chronic Damages due to extended abnormal weather (sea level rise, drought, etc.) become more severe compared to the 1.5°C scenario Long-term - *1

- This is indicated as “−” because it assumes a situation in which climate change responses are not adequately implemented.

- (Expected Impacts)

-

The risk of physical damage caused by natural disasters and abnormal weather due to climate change (physical risk) is expected to increase, and this risk could have an indirect impact on the business and finances of the borrowers to which we invest.

At the same time, transitional risks are assumed to be lower than in the 1.5°C scenario.

(ii) Selection of important sectors

Given the degree of climate change impacts and the scale of exposure of loans and bills discounted, we selected the electricity, real estate, automobile/automotive parts and oil/gas/consumable fuel sectors as important sectors for scenario analysis.

(iii) Organization of transmission channels for impacts on financial conditions of important sectors

We identified the transmission channels in which climate change impacts companies’ financial conditions in the important sectors in “the 1.5°C scenario” and “the 4°C scenario.”

In this process, we recognized important elements as listed in the table below.

[Key factors affecting each sector] Electricity sector Real estate sector Automobile/automotive parts sector Oil/gas/consumable fuels sector Transitional risk Policies/laws and regulations Introduction of carbon tax Introduction of carbon tax Introduction of carbon tax Introduction of carbon tax Technology Investments in R&D of low carbon technologies Investments in developing decarbonization-ready properties and others Investments in R&D of low carbon technologies Investments in R&D of low carbon technologies Market Changes in energy mix Shift of demand to environment-conscious properties Popularization of electric vehicles Changes in energy mix Reputation Changes in carbon neutral awareness of customers and communities Lower evaluations of non-environmentconscious properties Lower evaluations of cars with engines Changes in carbon neutral awareness of customers and communities Physical risk Acute Damage to power generation stations and others due to flood damage Damage to owned properties due to flood damage Damage to manufacturing sites due to flood damage Damage to oil refinery plants and others due to flood damage Chronic Suspension of electricity supply grids due to damaged facilities Lower labor productivity of workers due to global warming Suspension of production at manufacturing sites due to damage Suspension of oil refinery activities due to damaged facilities (iv) Quantitative assessment of transitional and physical risks in important sectors

In line with the transmission channels, we estimated each company’s financial statements by 2050. We calculated the increase in credit-related costs appropriate to the corporate credit strength changes derived from the resulting estimation.

[Transitional risk (1.5°C scenario)] Base scenario IEA-net zero emissions scenario Analysis target Exposure of loans and bills discounted for electricity, real estate, automobile/automotive parts sectors and oil/gas/ consumable fuel sectors Analysis period By 2050 Analysis method Estimate the impact on financial statements of companies in the target sectors of the transition to a decarbonized society and estimate the increase in credit-related costs Analysis result Around ¥3.0 billion (cumulative) [Physical risk (4°C scenario)] Base scenario IPCC-R8.5 Analysis target Exposure of loans and bills discounted for electricity, real estate, automobile/automotive parts sectors and oil/gas/ consumable fuel sectors Analysis period By 2050 Analysis method Hazard maps were created for business assets owned by companies in the target sector, the impact of flood damage on financial statements was estimated, and the increase in credit-related costs was estimated Analysis result Insignificant amount (v) Scenario analysis results

For key sectors, the transitional risks amount to a cumulative total of around ¥3.0 billion by 2050, while the physical risks are estimated to be an insignificant amount, meaning that the financial impact of either is likely to be limited.

-

As of March 31, 2025, carbon-related assets accounted for 29.3% of total loans*2.

Based on TCFD recommendations, loans to the energy, transportation, materials and construction, and agriculture, food, and forest products groups are defined as carbon-related assets.

- *2

- Total direct lending to members (shinkin banks) and non-members (¥9,111.1 billion)

<Dependence and Impact on Natural Capital>

- (1)The relationship between

shinkin banks and natural capital

The SCB depends on, and has an impact on, natural capital through its business activities.

Therefore, we believe it is necessary to analyze our relationship with natural capital and appropriately identify risks and opportunities. - (2)Analysis of our relationship

with natural capital

- (i) Dependence and impact on natural

capital at our places of business

We examined the points of contact between the places of business of the SCB and sensitive locations in natural capital from the five perspectives recommended in the TNFD recommendations.

The examination revealed some overlaps with sensitive locations. However, these were all relatively low-priority natural conservation areas, and the impact of the SCB’s business activities on sensitive locations is small.

Therefore, it has been concluded that there are no important area for the SCB. - (ii) Scope of

analysis

To identify risks and opportunities related to natural capital, we conducted an analysis in accordance with the LEAP approach recommended by the TNFD recommendations.

We selected loans and bills discounted as exposure to be analyzed. -

(iii) Dependence and impact of the loan

portfolio

Using “ENCORE,” we assessed the dependence and impact on natural capital across the entire loan portfolio for potentially important sectors (the 12 sectors outlined in Annex 1 of the Sector Guidance - Additional Guidance for Financial Institutions published by TNFD).

Specifically, we categorized sectors based on loan balances and the dependence and impact on natural capital, and identified sectors that should be addressed with greater priority.

As a result, 5 sectors—materials, real estate management and development, transportation, consumer services, and utilities—were identified as having large loan balances and significant dependence or impact.

- (i) Dependence and impact on natural

capital at our places of business

[Dependence on and impact of natural capital]

We have identified the dependencies and impacts on natural capital in the value chains taking our borrowers into consideration, for the five priority sectors with high dependence and significant impact on natural capital and with large loan balances.

Going forward, we will conduct detailed analyses, including the identification of risks and opportunities and proceed with the discussion on measurement, management and mitigation of risks that are important to the business activities of the SCB.

Risk Management

-

We manage climate change risks in the integrated risk management framework. Specifically, we recognize that these risks are causes of generating or amplifying risks in risk categories (such as market and credit risks).

We add climate change events to a risk map that classifies and organizes risks based on two criteria: “impact on the SCB” and “probability of occurrence,” and visualize and share them.

The risk map is reviewed, and revisions are approved as needed in the regular Risk Management Committee, which comprises executive officers and heads of relevant departments.

We respond to risk events according to their impact and likelihood.

-

We have distinguished those sectors whose financial conditions are susceptible to climate change and formulated the “Guideline for Responsible Investments and Loans by Type of Business.”

By making investments and loans in accordance with this Guideline, which is continually being revised, we are contributing to the realization of a sustainable society as well as managing the financial impact on the SCB.

[Outline of the Guideline for Responsible Investments and Loans by Type of Business] Name of business Businesses in which investment and financing are prohibited Across all businesses - Businesses that have negative impact on wetlands designated under the Ramsar Convention

- Businesses that have negative impact on World Heritage Sites designated by UNESCO

Specific business - Cluster munition manufacturing businesses

- Coal-fired power generation projects where the funds are used for the construction of new coalfired power plants

- Coal mining projects in which funds are used for the development of new coal mines for general coal mining and the expansion of existing coal mines, as well as coal mining using the Mountain Top Removal (MTR)

Businesses that require careful investment and financing Specific business - Oil and gas development businesses

- Large-scale hydroelectric power plant businesses

- Palm oil farm development businesses and deforestation businesses

-

The SCB adopted the Equator Principles in April 2021.

Based on these principles, we have established an internal management system and evaluate environmental and social impacts of projects in the decision-making process on project finance, etc., and continuously monitor those developments even after the project begins operation.

-

In the framework of credit screening, the impact of ESG factors on the creditworthiness of the customer is qualitatively evaluated, and credit decisions are also made based on the evaluation results.

In addition, when investing in funds, we evaluate the ESG investment stance of the entrusted asset management company and make investment decisions based on the evaluation results.

- For the natural capital risks, we will continue to investigate them.

Metrics and Targets

-

We have set a target of ¥5 trillion for the cumulative amount of sustainable finance from fiscal 2021 to fiscal 2030.

The scope of sustainable finance includes the finance (investment, loan, origination of project finance and syndicated loans, bond underwriting, fund formation, and fundraising) that contribute to tackling environmental and social issues, based on international principles and government guidelines.

[Amount of sustainable finance executed*1] Target Cumulative total of ¥5 trillion from fiscal 2021 to fiscal 2030 Result Cumulative total of ¥2,384.0 billion from fiscal 2021 to fiscal 2024 - *1

- Figures for the SCB Group are stated. This includes investments and loans totaling ¥323.6 billion provided by the SCB alone to the environmental sector.

-

To contribute to “carbon neutrality by 2050,” as outlined in the Paris Agreement and by the Japanese Government, the SCB Group has set a target to reduce greenhouse gas emissions (Scope 1 and Scope 2)*2 to virtually zero by fiscal 2030.

Based on the road map target, the SCB, which accounts for the majority of emissions, has divided its initiatives toward carbon neutrality into two phases: Phase 1, which is up to fiscal 2025, and Phase 2, which begins from fiscal 2026. We set staged targets for each phase and is implementing various measures around the three pillars of “decarbonization,” “energy-saving,” and “energy creation.”

In Phase 1, the goal is to reduce greenhouse gas emissions to 2,000 t-CO2 or less by fiscal 2025. To achieve this, in addition to continuous introduction of renewable energy-sourced electricity (green power), we have engaged in such activities as conducting pilot tests for carbon-offset city gas, engaging external agencies to perform energy efficiency diagnostics for data centers, and conducting design work for construction of ZEB (Net Zero Energy Building) stores aimed at reducing energy consumption within buildings.

Looking ahead to the further expansion of our initiatives beyond fiscal 2025, we plan to implement concrete measures toward achieving carbon neutrality, including the full adoption of green electricity at our own facilities and the enhancement of air conditioning systems for higher energy efficiency.

- *2

-

Scope 1: Direct emissions generated by the business operator itself

(combustion of fuel, etc.)

Scope 2: Indirect emissions generated through use of electricity, etc. supplied by another party - *3

-

Figures for fiscal 2021–fiscal 2023 represent the emissions from the SCB

alone.

Figure for fiscal 2024 represents the emissions from the SCB and its group companies in Japan.

-

We have set targets for reducing the balance of investments and loans used to finance the construction of coal-fired power plants by 50% by fiscal 2030 from the end of fiscal 2020 and to zero by fiscal 2040.

[Balance of investments and loans used to finance the construction of coal-fired power plants*4] Target Reduce by 50% by fiscal 2030 from the end of fiscal 2020*5and to zero by fiscal 2040 Result Balance at the end of fiscal 2024: ¥4.6 billion - *4

- Represents the balance for the SCB alone.

- *5

- Balance at the end of fiscal 2020: ¥5.9 billion